The demand for DOT117J railcar leases is expected to rise slightly in 2019, driven largely off an expected increase in overall freight rates and a more balanced railcar inventory mix as a result of the implementation of DOT117J regulations. However, the overall demand will depend heavily on what oil ends up doing in 2019 which is far from certain. All eyes will be on OPEC throughout 2019 to determine whether oil production and subsequent crude by rail (CBR) volumes will increase, driving leasing demands along with them.

Background on DOT117J Railcars

Almost 4 years ago, the DOT implemented DOT117 regulations to address safety concerns for railcars transporting flammable liquids such as crude oil, ethanol and other flammable petroleum products. The new regulations apply to non-pressurized tank cars and require jacketed and thermally insulated shells of 9/16-inch steel, full-height half-inch-thick head shields, sturdier, re-closeable pressure relief valves and rollover protection for top fittings. The first deadline to transition to new DOT117 regulations passed this year. However, the railroads are implementing incentives to shippers to upgrade their fleets ahead of the regulatory deadlines. – TG this is also below on page 5

New tank cars compliant with this standard are labeled DOT117J while refurbished tank cars that now meet the new standard are labeled DOT117R.

Approximately 41% of cars in DOT117 service currently carry ethanol and 23% carry crude petroleum . The remainder carry a variety of flammable liquid derivatives or switch between products. The figure below summarizes the product mix as estimated by a Bureau of Transportation Statistics (BTS) survey.

Driving Forces

Price (and supply) of Oil

The most significant driver of DOT117J railcar leases is the price of oil. As oil prices increase, production increases and with it, the demand for railcars. Recent delays and cancellations of prominent pipeline projects have cemented rail’s role in CBR transport, particularly from oil fields in the Dakotas and Canada.

Because oil demand globally increases in a fairly uniform and predictable way, oil prices depend heavily on global oil inventories. Generally, higher inventory levels result in lower oil prices. For example, when the fracking boom occurred in 2014, a rapid increase in production sent prices plummeting.

The Federal Reserve in St. Louis nicely illustrated this connection in the following chart :

Oil prices have had a rollercoaster 2018. After spending much of the year inching upwards as demand steadily rose, oil prices plummeted in October as OPEC agreed to increase production levels, raising inventories. As we look towards 2019, all eyes are on OPEC to see whether they will reverse course from the October decision and try to stabilize inventory levels. In early November, OPEC agreed to cut production by 1.2MM barrels. However, political discontent between OPEC members left the market skeptical of an agreement. A November 2018 WSJ article referred to “serious political disagreements” among the members.

If OPEC is successful in reducing production levels and oil prices rebound, the leasing demand for DOT117J cars is likely to increase. If not, however, they may remain depressed and with it the demand for DOT117J cars.

Supply and Demand of Railcars

In general, leasing rates are determined by railcar availability which can be visualized at a high level as:

New car deliveries – retirements + new freight growth = surplus/deficit of rail cars

Substantial fleet build-ups over the last few years due to low costs of capital and a booming fracking market have created a temporary oversupply of railcars since freight rates slowed in recent years. In parallel, concerns about regulatory changes have left lessees wary of agreeing to longer lease terms. The result has been several years of low lease rates.

The visual from the WSJ below illustrates this tension that’s characterized the segment for the last few years :

However, 2019 may finally see that balance shift. In a November 2018 article, Railway Age reported that research firm Cowen & Co estimates approximately 58,000 railcars DOT117J and DOT117R will be produced in 2019, largely due to replacements of DOT111 and CPC1232 rail cars. Demand is also expected to increase somewhat as freight rates are forecast to increase in 2019 and a smaller portion (~11,000 railcars) of the production will come from increasing overall petroleum shipments .

As the balance of railcars begins to even, we may begin to see increases in leasing rates, but likely without a capacity crunch. If oil prices regain their strength, leasing will continue to provide strong operational flexibility for fleet owners.

New Regulations on tankcar transporting oil DOT117J

Regulation continues to be a driving force in the demand for DOT117J cars.

In May of 2015, the DOT’s Pipeline and Hazardous Materials Safety Administration (PHMSA) and Federal Railroad Administration (FRA) passed Hazardous Materials: Enhanced Tank Car Standards and Operational Controls for High-Hazard Flammable Trains (HM-251) which required high-hazard flammable trains (HHFT) to upgrade their tank cars. The subsequent FAST act set a timeline for this transition. Significant progress has been made on transitioning the fleet to the new cars with the Bureau of Transportation Statistics (BTS) reporting that 20% of cars transporting class 3 flammables are now compliant with DOT117, compared with 2% in 2015.

The following table from the BTS shows the timeline required by the FAST act for transition to DOT117 compliant tank cars:

While the timelines for some products like Ethanol remain a few years out, Railway Age reports that some railroads are incentivizing fleet owners to change to the new DOT117J cars sooner by implementing taxes on rail cars that are non-compliant. These incentives combined with the existing timelines will continue to increase demand for DOT117J leases in 2019.

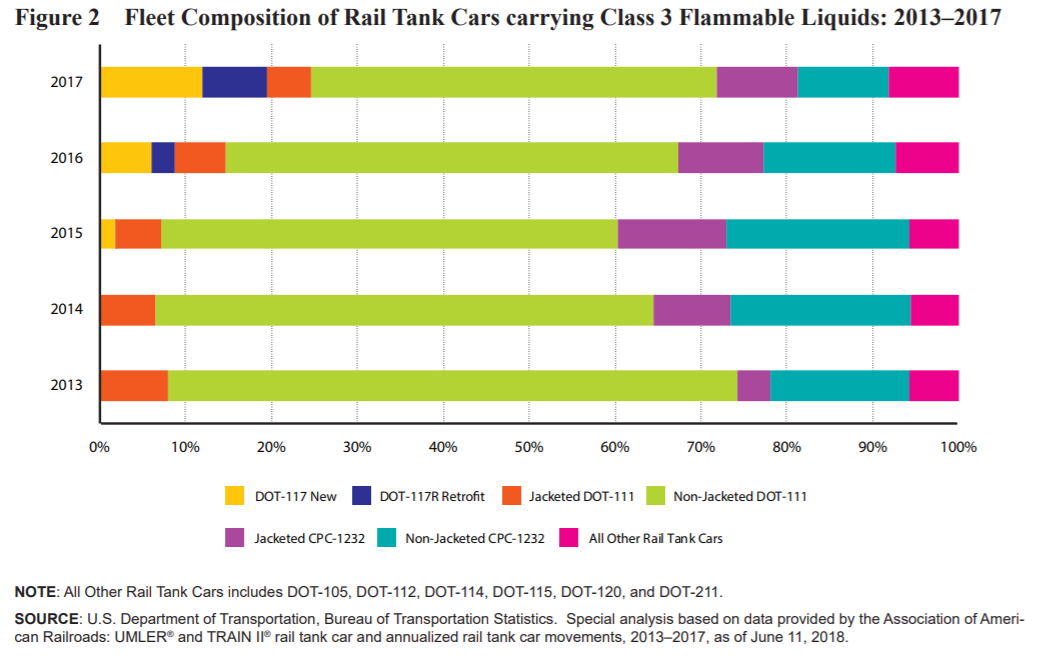

An estimated 40-75,000 cars remain candidates for retrofits. The BTS chart below shows the remaining fleet:

Generally, lessors cover the upfront cost of modifications to railcars to bring them into compliance with DOT117 standards. Lessees then pay a certain amount per month for the modification. As a result, leasing will be somewhat more attractive than purchasing to reducing the upfront capital costs that Railcar owners may have to spend to meet the regulatory compliances.

Financial exposure to railcar owners

Unable to secure the capital required to purchase a railcar outright, railcar users over the last several decades have found that leasing has been an attractive equipment sourcing solution

As inflation increases, the Federal Reserve has steadily increased interest rates and most experts expect this trend to continue in 2019. Rising interest rates may dampen some investment, but they also create a more favorable market for leasing. While lease rates can vary with interest rates, they also give operators far more financial flexibility. Rather than a 10-20 year depreciation schedule and a set rate loan, leasing terms are typically 5-7 years. High interest rates also make purchases of used (secondary) railcars less attractive, again driving the market towards leasing.